2000s: insurance continues to expand in emerging markets

Article information and share options

The concept of calculating exposures to certain dangers and risks and sharing the losses amongst as many people as possible has existed at least since the 18th century. During the 19th century, insurance, as it has come to be known today, first gained traction in Europe before expanding to the rest of the world. When sigma began tracking worldwide premium developments in the late 1960's, Europe and North America accounted for virtually all of the world's premium volume. At that time, almost half of the world's population lived in Asia, yet the region only accounted for roughly 6% of global premiums.

Over the last 50 years, advanced markets have continued to generate the highest premium volumes, but since the turn of the century, the emerging markets, especially China, have represented an ever-increasing share of global premium volume.

Slowdown of advanced markets

In the early 1980s, sigma shifted from tracking and analysing multi-year premium growth to looking at one year at a time. In 1984, when sigma reported on world premium developments in 1982, it split the world into three regions that dominated the global market at that time: North America, the European Community and Japan. Premiums in the "Rest of Europe" and Oceania were reported separately. In addition, Latin America, Asia (excluding Japan) and Africa were grouped under "Other countries". Together, they accounted for a mere 5.7% of world premiums.

Table 1: World premium volume 1982

Source: sigma No 4/1984

A closer look, however, revealed that premium growth in the Western economies was slowing down. Some insurance markets, such as Canada, the Netherlands and Ireland were even shrinking. Denmark had the largest negative growth in 1982 at -7.1%, while North Korea had grown the fastest at 52.4%.

In 1991, sigma reported that growth rates the world over had halved. The global slowdown was attributed to negative developments in the US and Japan. More than half of the 31 markets that had shown growth rates above 5% were outside of Europe and North America. Meanwhile, growth in Latin America and Asia was strong.

Growth in emerging markets begins to accelerate

In 1994, sigma began using the term emerging markets for Asian insurance marketsi. While Asia set out on a path of unprecedented growth, Latin America stagnated and Africa lagged behind. With the fourth edition of sigma in 2000, sigma began regularly devoting an issue to trends in the emerging markets, covering a broad range of emerging market topics from agricultural insurance and Islamic insurance to micro-insurance.

The high growth potential of the emerging markets, sigma explained, was one of the main factors that attracted foreign insurers. Insurers also followed their clients who increased their footprint in emerging markets. Expanding into new markets brought certain benefits, such as diversification of the risk pool and improvements in efficiency. Within emerging markets, there was demand not only for cover, but also for foreign know-how and new products that could be launched after markets were deregulated and the General Agreement on Trade in Services (GATS), a treaty of the World Trade Organization (WTO), was introduced.

Privatisation of social security in Asian markets became one of the main drivers for growth. Established western life insurers had an advantage over younger local companies due to their reputation as financially sound companies. A favoured strategy to enter new markets was through acquisition of smaller local companies.

Emerging markets rebounded well after crises

Such expansion was not without risks. In 2003, sigma dedicated an issue to analyse Mexico's Tequila Crisis in the mid-nineties, the Asian Crisis in 1997 and Argentina's Tango Crisis in the early 2000s. This reminded many that growth could not be taken for granted. According to sigma, insurers face certain consequences after a financial crisis. Demand for insurance usually falls due to the decline of total economic output. At the same time, surging inflation often drives up claims. The latter is aggravated by the fact that premium income usually lags inflation, but claims increase because of higher prices. In addition, the value of invested assets often falls due to rising interest rates.

One of the conclusions from a 2005 edition of sigma that focused on liability developments in emerging markets was that "Increasing globalisation, regional economic cooperation, inflows of foreign direct investment and changes in the legal and corporate sphere" favoured the development of liability lines. Liability business was especially exposed to risks as inflation demanded higher reserves, which could put insurers' solvency at risk.

While the outlook for liability business was deemed overall positive, the authors cautioned that emerging markets might follow "worrisome trends" in industrialised markets, especially the "escalating loss environment in the USA". If emerging markets were to adapt their liability regimes to US standards, the industry would risk major disruptions.

Yet, overall optimism prevailed, especially for the two largest markets in Asia: China and India, nicknamed the dragon and the elephant. In a 2011 edition dedicated to emerging markets, sigma noted that domestic life companies in some markets had access to better distribution networks. In a later issue, sigma concluded that with the introduction of bancassurance in both China and India in 2001, new market entrants could now gain access to clients more easily.

In 2007, the global financial crisis, which initially affected the US and European markets, began to reverberate around the world. The crisis came ahead of the planned introduction of more stringent legislation for capital requirements in Europe.

The US-inspired risk-based capital (RBC) approach was introduced 1994. Regulators in emerging markets slowly adopted it, with Singapore, Indonesia and Taiwan among the early adopters. The European Solvency II approach, which first went into effect in 2016, went further in terms of capital requirements. Initially, there were concerns that it could potentially create a disadvantage for European insurers in emerging markets.

Micro- and indemnity-based insurance

While some emerging markets caught up with advanced markets in terms of purchasing power parity already in 2007/2008, insurance products remained out of reach for many individuals in less developed markets.

A 2010 sigma addressed micro-insurance, an alternative form of serving the low-income population. Micro-insurance, a new type of insurance based on micro-credit models, had already been introduced in the 1990s. It garnered attention, not only with the United Nations' International Year of Microcredit in 2005, but also because it coincided with a general trend to put more emphasis on improving financial resilience rather than post-disaster financing. By using alternative distribution channels such as mobile phones and targeting "aggregator organisations" such as farmers' associations, insurers reduced operational costs, making ex-ante insurance solutions more affordable.

Because loss assessment proved cost-intensive, new products were developed that introduced automated claims payments tied to a loss index. These products also helped mitigate moral hazard, adverse risk selection and fraudulent claims.

Takaful insurance: an alternative to conventional insurance

Insurance products for the Muslim population, which have existed since the 1970s, did not gain much traction until the 2000s. In a 2008 edition on Islamic insurance, sigma estimated that "around 1.5 billion Muslims around the world are underserved by the insurance sector". The study went on to explain that according to Islamic jurists, conventional insurance was not aligned to the shariah, the body of Islamic law.

Takaful insurance offered an alternative as it was based on the principle of mutual assistance and voluntary contribution, where the risks were shared collectively. To grow, takaful faced certain obstacles, which included the shortage of Islamic investment opportunities, the lack of liquid markets for Islamic bonds in different regions and the shortage of takaful reinsurance capacity. Insurance expertise combined with shariah expertise was also lacking.

Current and future outlook for emerging markets

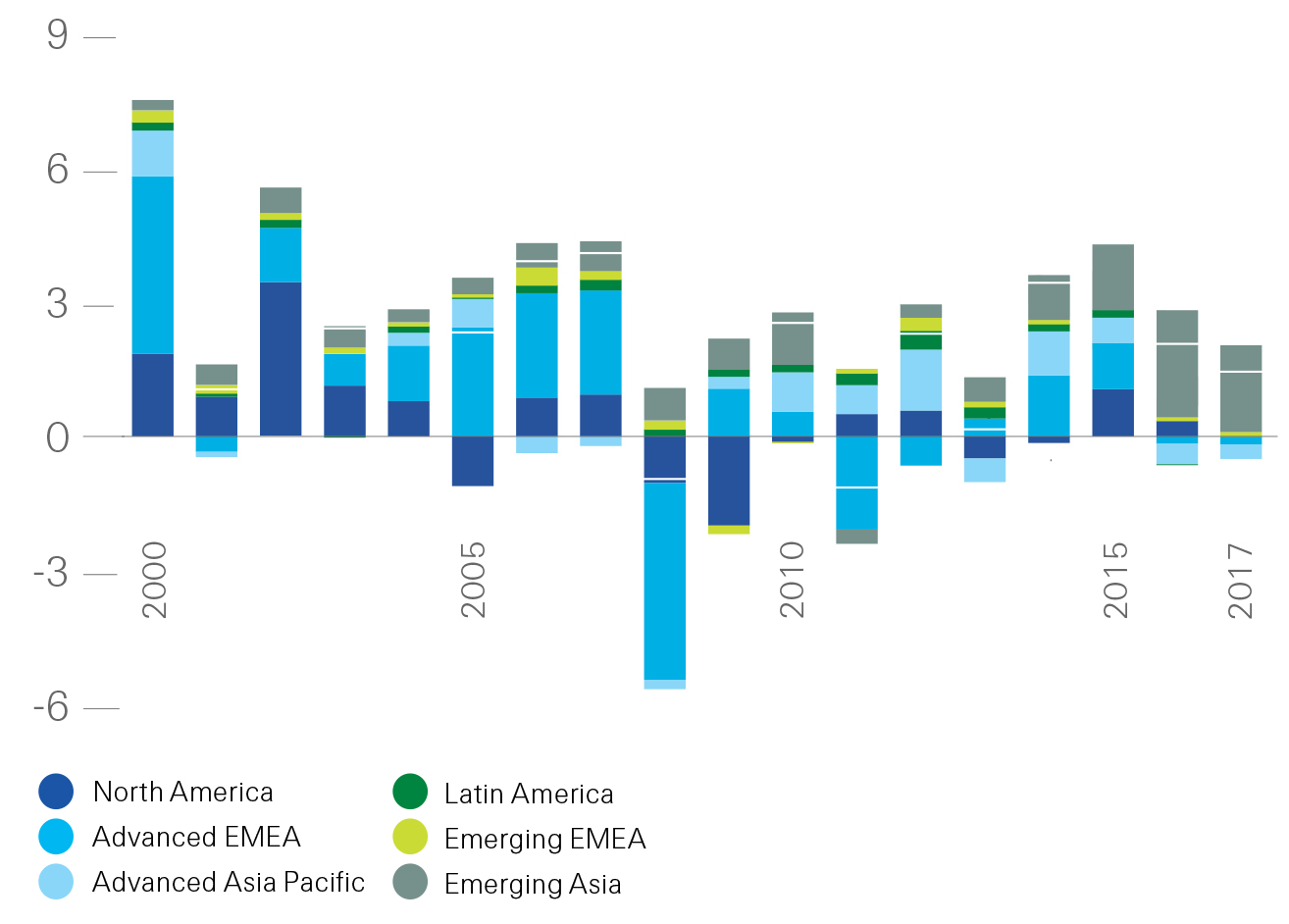

Since the financial crisis, emerging markets have continued to outperform the advanced markets in terms of growth rates. For the past few years, emerging Asian countries, and in particular China, have been the biggest growth engine. However, other regions have grown as well. The market share of emerging markets has risen to 22% in 2017 and it is likely to continue over the next decade as many economies continue to grow strongly and insurance markets become more mature.

Figure 1: Contribution of main regions (in percentage points) to total real premium growth (in %; indicated by white line for years with negative regions), 2000‒2017

Source: Swiss Re Institute, sigma No 3/2018

In the shorter term, China is likely to become the next Japan for insurance market growth, given the recent steep increases in penetration levels and strong economic growth. Due to the sheer size of its population and the economy, China will remain the biggest contributor to global insurance market growth among emerging markets for the next decade at least. However, fifty years from now, when sigma celebrates its 100th anniversary, the world‘s fastest growing insurance market could be India, Indonesia, Brazil, Mexico, Pakistan, Nigeria or Ethiopia. Only time will tell.

While economic development is expected to support growth, the protection gap is still large in emerging markets. This is not only in respect to natural catastrophes, but also in areas such as life mortality and health, where there is room to improve cover and close the protection gap.

References

iThe designation of the economies in this sigma as “advanced” or “emerging” is generally in keeping with the conventions of the International Monetary Fund (IMF). Advanced economies include the US, Canada, Western Europe (excluding Turkey), Israel, Oceania, Japan and the other advanced Asian economies (Hong Kong, Singapore, South Korea and Taiwan). All other countries are classified as “emerging” and generally correspond to the IMF´s “emerging and developing” economies